Liquidity Planning: Guide, Example & Template for 2026

In this guide, you will learn step by step how to create a liquidity plan, which mistakes you should avoid and why 13-week planning is becoming standard. With a specific example, template and practical tips.

The most important things in brief

- Liquidity planning shows you whether your company Able to pay at any time stays and warns you of bottlenecks in good time.

- In five steps, you create a liquidity plan: 1. Starting balance → 2. Payments → 3. Payments → 4. Balance → 5. Final balance.

- Particularly at risk of liquidity bottlenecks: micro-enterprises. 81.6% of all insolvencies According to Creditreform, affect companies with less than 10 employees.

- The 13-week liquidity plan (Rolling Forecast) is the gold standard of short-term financial planning. It achieves over 95% forecast accuracy in the first 4 weeks and is required as a minimum standard by banks and restructuring consultants (gTreasury, 2025).

- Excel is enough to start but quickly reaches its limits: no real-time data, no automatic bank connection, prone to errors when entered manually. Specialized liquidity planning tools such as Tidely automatically sync account data and reduce weekly time by an average of 51%, which corresponds to around 4 hours (Tidely user survey).

- Update your liquidity plan at least weekly. Or use a tool like Tidely.

What does liquidity planning mean and why is it important?

Liquidity planning is the structured comparison of all expected deposits and withdrawals over a defined period of time. It shows you at a glance how much money is available in your account at what time.

23,900 corporate insolvencies in Germany in 2025, which is the highest level in over ten years. Estimated total loss: 57 billion euros. 285,000 jobs affected. The most common cause is not a lack of innovation, but simply: no more money in the account. These are the figures from Creditreform.

Since the low point caused by the COVID insolvency moratorium in 2021 (13,990 cases), insolvencies have risen by over 70%. 43% of German companies rate their financial situation as problematic. As many as not since the pandemic, reports the German Chamber of Industry and Commerce (DIHK). Two years of recession have consumed the reserves of many companies. A further increase to around 24,500 cases is forecast for 2026 (Allianz Trade).

Clean liquidity planning protects against this. This doesn't require a degree in controlling, but a tool that shows you whether you can still pay salaries next month or whether you need to act now.

Definition: What is a liquidity plan?

The liquidity plan (also: liquidity forecast or cash flow planning) shows the result as a balance: positive means solvent, negative means need for action.

Unlike the profit and loss statement (P&L), liquidity planning does not look at income and expenses. It only records actual money movements. A company can be profitable and still become insolvent if customers pay too late or large expenses lower the account balance faster than income flows back.

Reading tip: Basic knowledge of liquidity and liquidity calculation

Accrual: Liquidity Plan vs. Financial Plan

The financial plan is the big picture: investments, financing and long-term capital structure. The liquidity plan is operational: It focuses on daily or weekly solvency. Both belong together, but the liquidity plan is the early warning system.

Imagine the financial plan as a map and the liquidity plan as a fuel gauge for your car. The map shows you where you want to go. The fuel gauge tells you whether you have enough gas to get there.

For whom is liquidity planning particularly important?

In short: Liquidity planning makes sense for every company with more than one employee. It is required by law for corporations (StaRUG); for micro-enterprises without their own financial department, it is the most important protection against insolvency.

Liquidity planning makes sense in principle for every company with more than one employee. Liquidity planning is mandatory for corporations and larger companies anyway: The StaRUG requires an early warning system to identify developments that jeopardize their existence, and banks regularly require a 13-week preview during loan negotiations.

But it is essential for the survival of micro-enterprises in particular. 81.6% of all insolvencies in 2025 affected companies with up to 10 employees. That's around 19,500 tradesmen, restaurateurs, freelancers and small agencies, i.e. companies that often do not have their own controlling department (Creditreform, 2025).

Without planning, a late payment quickly becomes a liquidity bottleneck. Large companies have credit lines and financial teams to absorb this. Not micro-enterprises. That is exactly why they need simple, pragmatic liquidity planning the most.

Good to know: Since January 2021, the Corporate Stabilization and Restructuring Act (StaRUG) has required managing directors of corporations (GmbH, AG, UG) to set up an early warning system for developments that threaten their existence. Documented liquidity planning fulfills this obligation. Without it, managing directors risk personal liability in the event of insolvency.

The most common causes of insolvency

Late customer payments, unexpected costs, and seasonal fluctuations are the three main drivers. Insolvency rarely occurs overnight. It is the result of a chain in which a lack of visibility into one's own payment flows is the decisive factor.

In the US, 56% of small businesses are affected by outstanding invoices, with an average of $17,500 per establishment. 47% have invoices that have been outstanding for over 30 days. This is shown by the QuickBooks Late Payments Report from 2025. The figures are likely to be similar in Germany.

45% of small businesses with fewer than 19 employees report financing difficulties (DIHK, 2025). Anyone who does not have a clear overview of their liquidity cannot submit a convincing loan application to the bank.

Industry risk: Not all industries are affected equally

Transport and logistics keep insolvency statistics with 12.3 cases per 10,000 companies. Followed by hospitality (10.5) and construction (8.5). The average is around 6.1. In December 2025, regular insolvencies rose by a further 15.2% compared to the previous year (Destatis).

In high-risk industries, liquidity planning is not optional but mandatory. But even in less affected industries, visibility of your payment flows is the best protection against unpleasant surprises.

Tidely industry solutions: gastronomy · ecommerce · retailing · agencies

Equity as a buffer: Is that enough?

A high equity ratio sounds reassuring, but says little about actual solvency. The decisive factor is not what is on the balance sheet, but what is available in the account. That is exactly what liquidity planning shows.

The average equity ratio in SMEs is 30.7% (KfW SME Panel, 2025). But 28.4% of SMEs are undercapitalized with less than 10% equity. 6% have negative equity. For these companies, a single bad month can be life-threatening.

Equity is on the balance sheet but not in the account. Machinery, warehouses, receivables: All of this is equity, but it won't help you if salaries are due on the 15th.

Reading tip: Avoid liquidity bottlenecks: How to protect your company

How do I create a liquidity plan? Step-by-step guide

A liquidity plan is created in five steps: enter the initial balance, plan payments, plan payouts, calculate the balance, determine the final balance.

You don't need any software for that. A spreadsheet or even a sheet of paper is enough to get you started. According to the KfW SME Panel (2025), only 39% of SMEs implemented investment projects in 2024. Many act out of fear instead of strategy. A liquidity plan gives you the data basis for well-founded decisions.

Step 1: Enter initial inventory

Record the current balance of all business accounts. That is your starting point. Only money that is actually available counts, not granted but unused credit lines.

tip: Always use Monday as the deadline for a clean weekly rhythm.

Step 2: Plan deposits

List all expected cash receipts:

- Sales revenue (receipt of payment, not invoice date!)

- Receivables from outstanding invoices

- Refunds (input tax, insurance)

- Loan or funding disbursements

- Other income (rental income, interest)

Plan conservatively. If a customer pays “in 14 days,” expect 30 days. 56% of small businesses are struggling with late payments (QuickBooks, 2025). Nothing is more dangerous than optimistic revenue assumptions.

Step 3: Schedule payouts

Record all planned expenses, sorted into three categories:

Fixed costs (every month):

- Salaries and social security contributions

- Rent and additional costs

- insurances

- Credit rates and interest

- Software subscriptions

Variable costs (fluctuating):

- Purchase of goods and materials

- marketing and advertising

- travel expenses

- Freelancers and service providers

Periodic costs (not monthly):

- Advance VAT payments (monthly or quarterly)

- Business tax prepayments

- Income tax prepayments

- Annual insurance premiums

Step 4: Calculate balance

Deposits minus withdrawals result in the balance for the period.

A positive balance means more money in than out. A negative balance is no reason to panic as long as the final inventory remains positive. But it's a warning sign.

Step 5: Determine final inventory

Starting inventory plus balance results in the final inventory.

The end inventory of one period becomes the start inventory of the next. This creates a chain that shows how your liquidity is developing. Define a critical threshold, such as two months of fixed costs. If the final inventory falls below this, this is your alarm signal.

Liquidity planning example: A template to imitate

Allianz Trade predicts around 24,500 insolvencies in Germany for 2026. So that you don't belong, here is a specific example to imitate. Our example company: “WebAgentur Müller GmbH”, a service provider with 8 employees, approx. 45,000€ monthly turnover and 32,000€ fixed costs.

Sample liquidity plan: January to March

What does this example tell us?

The final inventory falls from 25,000€ to 11,000€ in two months. Not yet critical, but a clear signal. An additional back business tax payment of €5,000 in February would have reduced the buffer to €6,000. Well below the two-month threshold.

In March, the balance turns positive. Typical for project-based companies: Incoming payments lag behind the performance period. The agency worked in January but the bill won't be paid until March.

From practice: The most dangerous months are not the weak sales. These are the months in which large expenses (tax advance payments, annual insurance) meet late customer payments. A liquidity plan makes exactly these collisions visible weeks before they become a problem.

Summarized: A liquidity plan example shows: Even with a monthly turnover of €45,000, the account balance can fall from €25,000 to €11,000 in two months. The biggest risk is months in which high fixed costs meet late payments.

Typical tripping hazards

- Turnover is not the same as liquidity. You can be working at full capacity and have no money in your account.

- Taxes are often forgotten. Advance VAT payments and business tax rise quarterly and often unexpectedly.

- Seasonal fluctuations are ignored. Many industries have months with significantly less income.

- One-off costs are overlooked. Annual insurance, license renewals, hardware: Everything can be planned, but is often forgotten.

Download: Free Excel template for your liquidity planning

Why 13 weeks? Rolling liquidity planning explained

In short: The 13-week rolling forecast is the gold standard for short-term liquidity planning. It achieves over 95% accuracy in the first four weeks (gTreasury, 2025) and is required as a minimum standard by banks, restructuring consultants and the StaRUG.

In weeks 5 to 8, it is 85 to 90%, in weeks 9 to 13 it is 70 to 85%. This makes the rolling forecast the most precise instrument for short-term solvency.

This is how the rolling forecast works

You always plan exactly 13 weeks ahead. Each week, the oldest week is omitted, and a new one is added at the end. This gives you a permanent overview of the next three months, which automatically adapts to reality.

Why exactly 13 weeks? Because that equates to a quarter. Most business-critical cycles (tax prepayments, quarterly targets, credit installments) run quarterly. 13 weeks fully capture these cycles. You identify bottlenecks 4 to 8 weeks before they happen. Enough time to take countermeasures.

When is 13-week planning mandatory?

- renovations: The StaRUG requires integrated financial planning as mandatory proof.

- Credit negotiations: Banks regularly demand a 13-week plan.

- Shareholder disputes: The plan creates transparency as an objective basis for decision-making.

- Fast growth: Advances are rising, liquidity is paradoxically becoming scarcer.

From practice: 13-week planning is not a crisis tool. It is a growth tool. Proactively planning companies not only identify risks earlier, but also opportunities: excess liquidity for investments, favourable times for special repayments, optimal negotiation times for credit terms. Tools like Tidely are designed to do just that.

Liquidity planning in a business plan: What banks want to see

Banks and investors expect liquidity planning in the business plan for at least 12 months with three scenarios (Best, Base, Worst Case) Realism is crucial: incorporate seasonal fluctuations, start-up losses and buffers instead of planning consistently increasing sales.

According to the KfW SME Panel from 2025, 25% of German SMEs are thinking about closing their businesses. The other 75% often need a convincing business plan as the key to financing.

Two differences from operational planning:

- period: 12 to 36 months instead of 13 weeks.

- purpose: Demonstrate the viability of the business model, not just ensure short-term solvency.

What liquidity planning should include in the business plan:

- Monthly statement for at least 12 months

- Three scenarios (optimistic, realistic, pessimistic)

- Clear assumptions for each item

- Break-even month

- Determination of capital requirements

What banks pay particular attention to:

Banks pay particular attention to realism. Anyone who only plans to consistently increase sales appears naive. Anyone who plans for seasonal fluctuations, start-up losses and buffers appears prepared.

83% of medium-sized companies have an annual turnover of less than 1 million euros (IfM Bonn: SMEs in Germany, 2025). For these companies, a streamlined liquidity plan with 12 months and two scenarios is often sufficient. Complex DCF models are only common after financing rounds of over 500,000 euros.

A common mistake: Founders plan sales optimistically, but forget about payment delays. In Germany, 45% of all B2B invoices are paid late (Intrum: European Payment Report, 2024). Anyone who expects immediate payment in the business plan immediately loses credibility.

Practical tip for a bank appointment:

In addition to the business plan, prepare a separate 13-week preview. This shows the bank that you are not only planning for the long term, but also have operational control. Tidely automatically generates this preview based on your account details.

Excel vs. software: Which liquidity planning tool is right for you?

Automation reduces planning errors by up to 50%. Nevertheless, 50% of finance teams still rely on manual processes (gTreasury, 2025). The question is therefore not whether you need a liquidity planning tool, but when you will switch over.

When Excel is enough

Excel is a good place to start if you're just starting out, running a small business with one account, have less than 50 transactions per month, or don't have a budget for software.

The limits: no automatic bank connection, prone to errors when entered manually, no real-time data, no scenario comparison at the push of a button.

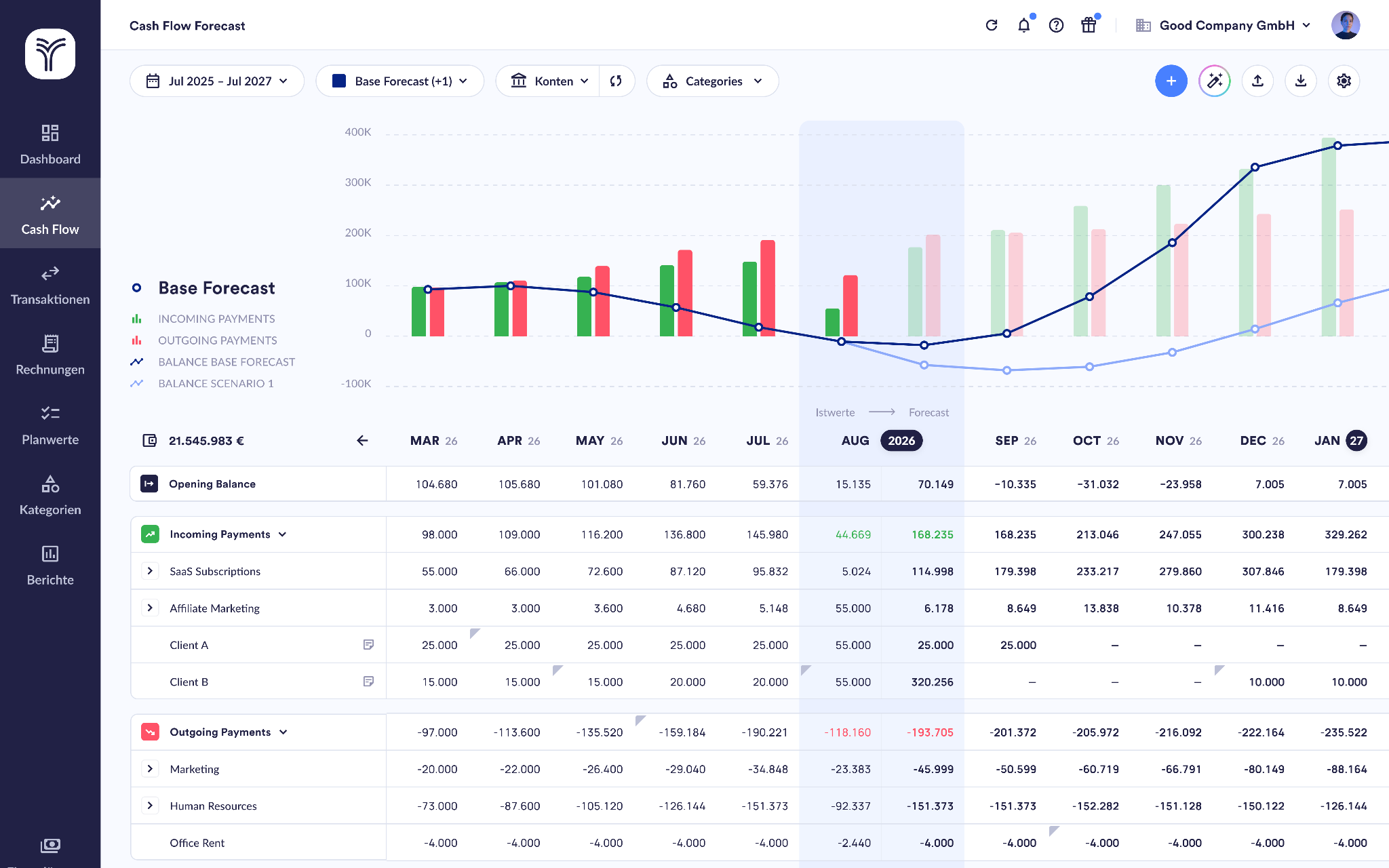

When a specialized liquidity planner like Tidely makes sense

A digital liquidity planner is worthwhile for 20 bookings per week, several bank accounts, first employees or the request for automatic updates. Tidely offers:

- AI-generated auto forecast: automatic liquidity forecast based on your historical cash flows

- Automatic bank connection: Connection to over 5,000 banks, ERP and accounting systems (DATEV, sevDesk, lexoffice, Billomat, etc.) with daily synchronization

- AI-based transaction categorization: Payments are automatically assigned to the correct categories

- Scenario comparisons: Create and compare best, worst and base cases with just a few clicks

- Automatic report generation: PDF and Excel reports at the push of a button

- Dashboard with real-time KPIs: daily overview of your entire financial situation

Tidely is developed in Germany, GDPR-compliant and ISO 27001 certified. The data is stored on German servers with bank-level encryption.

The tool connects directly to your bank accounts, automatically categorizes payments and shows liquidity history as an interactive dashboard. Via the DATEV integration, your open items (OPOS) sync automatically too, keeping receivables and payables up to date without manual exports. Scenario comparisons are made with just a few clicks instead of using complicated Excel formulas.

35% of SMEs are now using digitization projects, 20% are already using AI (KfW Digitalization Report, 2024). With Tidely, you can demonstrably save yourself time.

One user survey With 125 participants, shows:

- 73% of the companies surveyed are employed at least once a week with their liquidity planning.

- With Tidely, the time required for this is reduced by an average of 51% per week, which is approximately 4 hours corresponds.

- 85% of users plan to use Tidely after their subscription expires continue to use.

- The most used Tidely features are cash flow planning with scenarios (79%), the dashboard (53%) and the account overview (42%).

Reading tip: Top 10 liquidity planning software 2026

The 5 most common mistakes in liquidity planning

In short: The five most common mistakes in liquidity planning: confuse turnover with liquidity, forget tax deadlines, do not update the plan, do not include a buffer and only plan optimistically. A weekly 15-minute review prevents most of these mistakes.

16% of the planned investment projects were completely abandoned in 2024. A record figure according to the Kreditanstalt für Wiederaufbau (KfW). Not always because of a lack of money. Often because faulty planning created uncertainty that prevented better decisions.

Mistake 1: Conflate turnover with liquidity

80,000€ turnover in January sounds good. But if only 12,000€ actually arrives in the account because customers only pay in 30 to 60 days, you have a problem. Always plan the actual receipt of payment, not the outgoing invoice.

Mistake 2: Not scheduling tax appointments

Advance VAT payments, business tax, income tax advance payment, payroll tax: everything is regular, but rarely the same every month. Record all tax dates firmly in the plan. Many liquidity crises result from “forgotten” tax payments.

Mistake 3: Plan once and never update

A January plan that wasn't updated in March is worthless. 15 minutes a week for the plan/actual reconciliation. Friday afternoon, fixed date. This review is more important than initial planning.

Mistake 4: Don't include a buffer

Calculate a security buffer of 10 to 15% on the spending side. Or keep at least two months' fixed costs as a reserve. A broken machine, an back tax payment, an insolvent customer: without a buffer, every surprise becomes a liquidity bottleneck.

Mistake 5: Plan best case only

What happens if your biggest customer pays four weeks late? Always plan at least two scenarios: realistic and pessimistic. This costs 20 minutes more and can save your business.

Conclusion: Liquidity planning is your shield

23,900 insolvencies in 2025, 43% of companies with tight financial situations, 81.6% of those affected are micro-enterprises. These are the facts. Anyone who does not do liquidity planning is navigating blindly. A good liquidity planning tool makes the difference between control and crisis.

The good news is that it is neither complicated nor expensive. Five steps, a spreadsheet, 15 minutes a week. This gives you a better overview than most of your competitors. A liquidity planner like Tidely automates the process. For the next step, tools like Tidely help automate the process and run through scenarios at the push of a button.

What you should do now:

- Create your first liquidity plan using the template above.

- Download the free Excel template.

- Enter all tax dates for the next 13 weeks.

- Plan 15 minutes every Friday for the plan/actual reconciliation.

- Calculate your critical threshold (2× monthly fixed costs).

- Try Tidely free for 7 days.

Liquidity Planning FAQs

What is liquidity planning

Liquidity planning is the systematic comparison of all expected deposits and withdrawals over a specific period of time. It shows whether a company remains solvent at all times. With 23,900 insolvencies in 2025 (Creditreform), it is the most important early warning system for micro-enterprises, which account for 81.6% of those affected.

How do I set up a liquidity plan?

Five steps: (1) record the opening balance, (2) plan cash inflows, (3) plan cash outflows, (4) calculate the balance, (5) determine the closing balance. Plan conservatively: 56% of small businesses struggle with late customer payments (QuickBooks, 2025). Expect longer payment terms than agreed.

Why 13 weeks of liquidity planning?

The 13-week plan provides over 95% forecast accuracy in the first four weeks (GTreasury, 2025). 13 weeks correspond to one quarter and cover the most important payment cycles. Banks and restructuring advisors require this period as a minimum standard.

What is an example of liquidity?

€25,000 in the account, €28,000 in salaries due in five days, €15,000 customer payment expected. Liquidity as of the reporting date: 25,000 + 15,000 − 28,000 = €12,000. Sufficient. Important: liquidity does not equal profit. A profitable company can still be illiquid.

How accurate is a liquidity forecast?

The accuracy depends on the time horizon. With a 13-week plan, the hit rate in the first four weeks is over 95% (GTreasury, 2025). In weeks 5 to 8, it drops to 85 to 90%, in weeks 9 to 13 to 70 to 85%. Automated tools connected to banks achieve significantly higher accuracy than manual methods because they are based on real-time data rather than estimates.

However, many companies still use manual methods. As recently as 2022, a PYMNTS survey revealed that 72% of treasury managers manually prepare their cash flow forecasts (PYMNTS, 2022). A lot has happened since then: according to a recent study, 70% of companies now use at least one AI tool in cash management (PYMNTS, 2025).

In Germany, the AI adoption rate among SMEs is 20% (KfW: Digitalization Report for SMEs, 2024). The potential for automation is therefore significantly greater in the DACH region.

How often should I update my liquidity plan?

At least once a week. The plan/actual comparison takes 15 minutes and is the most important part of planning. High-risk industries, such as transportation, hospitality, and construction, with around 10,000 insolvencies per year, should check account balances daily (Destatis, 2025).

How much does liquidity planning software cost?

Most specialized liquidity planning software for SMEs costs between €45 and €200 per month, depending on the range of functions and number of bank accounts. By way of comparison, 35% of liquidity managers in German SMEs spend more than 10 hours per month on manual financial management (Innofact study via Deutscher Mittelstands-Bund). At an average hourly rate of €50, that is over €500 per month in personnel costs. Software such as Tidely therefore often pays for itself in the first month. Tidely offers a 7-day trial without a credit card.

What is the difference between liquidity planning and cash flow planning?

The terms are often used interchangeably but describe different perspectives. Liquidity planning focuses on solvency: can the company pay its invoices by the due date? Cash flow planning looks at the flow of money over a period of time: how much money flows in, how much flows out? In practice, the two overlap. A liquidity plan uses cash flow data as a basis but supplements it with account balances, credit lines, and due dates. For SMEs, the distinction is academic. The decisive factor is that you plan at all.

sources

- Creditreform Economic Research: Bankruptcies in Germany, year 2025

- DIHK: Economic survey at the beginning of 2025

- DIHK: Financial position of companies 2025

- Allianz Trade: Insolvency Study 2025

- Star UG: https://www.gesetze-im-internet.de/starug/__1.html

- Federal Statistical Office (Destatis): Bankruptcies 2025

- KfW: SME Panel 2025

- KfW: Digitalization Report for SMEs 2024

- KfW: Economic compass Q4 2024

- QuickBooks: Late Payments Report 2025

- gTreasury: 13-Week Cash Flow Forecasting 2025

- IfM Bonn: SMEs in Germany, 2025

- Intrum: European Payment Report, 2024

- PYMNTS/American Express: B2B digital payments tracker, 2022

- PYMNTS Intelligence/bottomline/FIS: Time to Cash — A New Measure of Business Resilience, 2025

- Innofact study via German SME Federation: Optimized liquidity management for SMEs

About the author

.jpg)

Niclas Storz is founder and CEO of Tidely, a B2B SaaS software solution for liquidity management for small and medium-sized companies. He previously worked as a management consultant for over 20 years. Most recently as Senior Partner & Managing Director at BCG.